rndfittool

Risk-neutral Density Fitting Tool (MATLAB)

Current version

v18.12

Author

Andrea Barletta

Latest downloads

MATLAB App installer v18.12 (recommended)

Zip archive containing all codes v18.12

Changelog

- [2018-12-12] Added support to CBOE new data format; Changed smoothing algorithm; Changed algorithm to fix slope/curvature; Optimized the implementation of positive mass constraints; Improved the iterative algorithm; Added information on PCA constrained optimization in the log window; Code polishing and other minor enhancements; Fixed a bug occurring when the string “rndfittool” appears in the name of the folder containing the main function; Fixed minor bugs in data exporting.

- [2017-18-12] Fixed compatibility on Unix systems; Addressed compatibility on Mac systems (needs testing).

- [2017-11-15] Improved numerical stability of the greeks computation algorithm; Fixed small bugs affecting plotting of greeks.

- [2017-08-28] Added model-free computation of options sensitivity with respect to variance-swap (VS vega); Fixed compatibility issue occurring on Unix systems.

- [2017-06-26] Fixed a bug producing bad plotting in Matlab most recent versions (>R2015b).

- [2017-04-27] Fixed a bug occurring when plotting greeks.

Getting Started

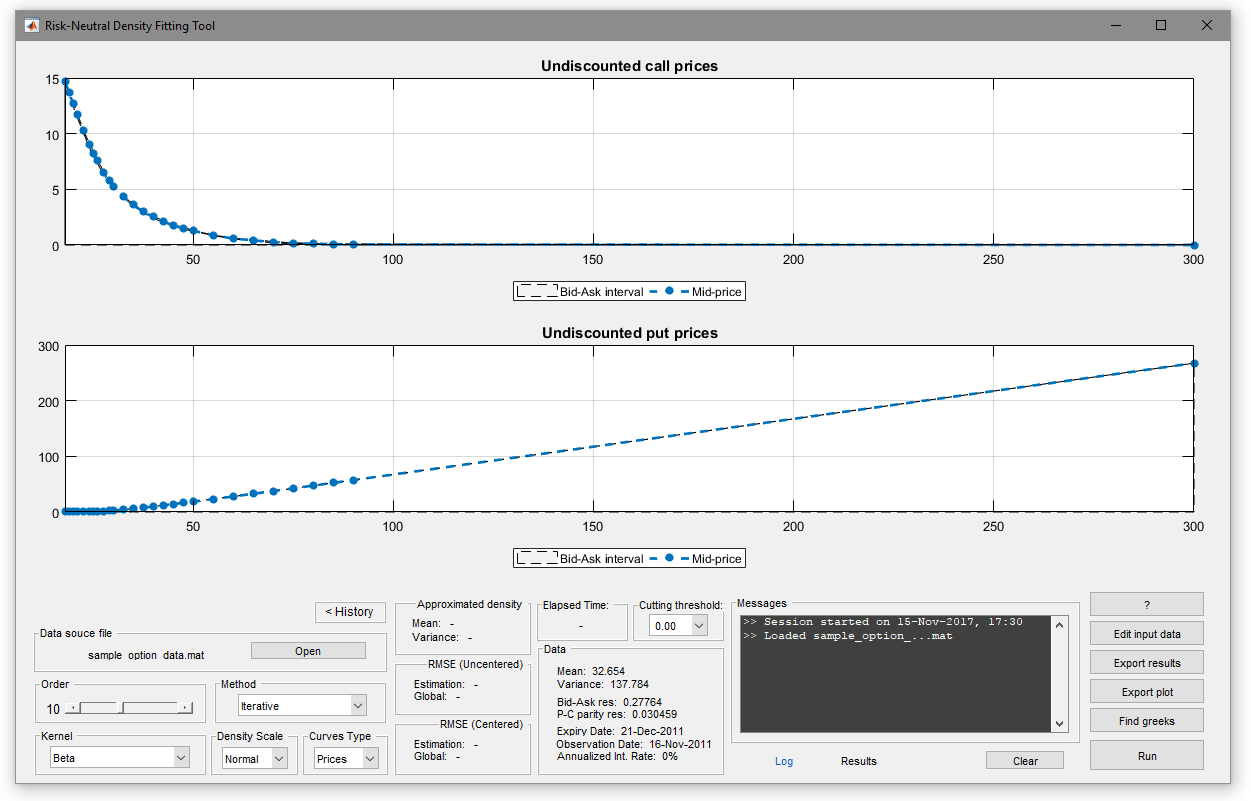

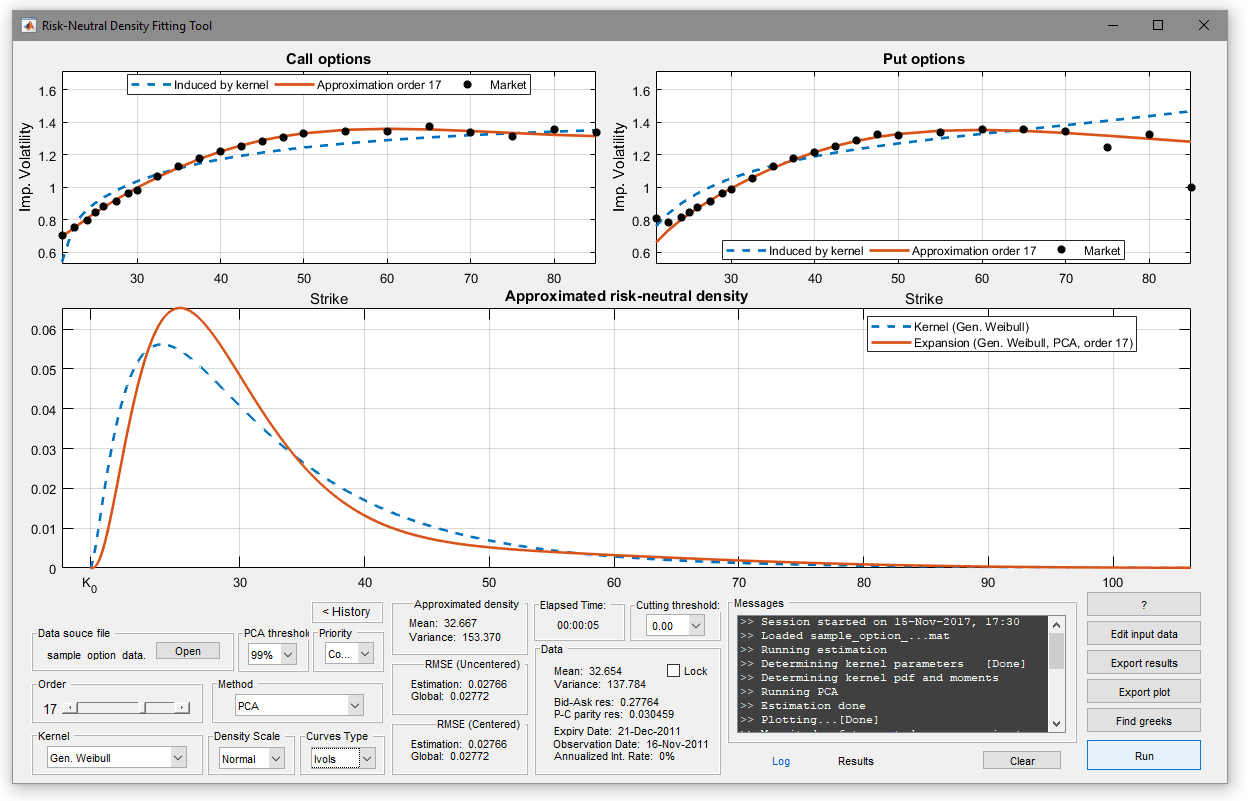

The Risk-neutral Density Fitting Tool tool (rndfittool) allows for inferring the risk-neutral density (RND) and the Greeks embedded in a set of observed call and put option prices. The underlying methodology is fully non-structural, meaning that it does not rely on any parametric model, and it consists in approximating the RND through orthogonal polynomial expansions. A detailed description of this methodology is provided in this paper (RND and moments) and in this paper (Greeks). Please note that this tool is not a standalone software, but it fully relies on the MATLAB suite.

Prerequisites

This code has been tested on MATLAB R2017a, R2016b, R2015b, R2014a and R2014b. However, there is a chance that it also runs on older versions of MATLAB. The following MATLAB Toolboxes are required to ensure full compatibility of the code:

- Curve Fitting Toolbox

- Financial Toolbox

- Optimization Toolbox

- Statistics and Machine Learning Toolbox

Installing rndfittool

There are two options to install the Risk-neutral Density Fitting Tool on your machine.

Installing rndfittool as MATLAB App (recommended)

- Download the MATLAB App installer.

- Double-click on the file to start the installation process.

- If the double-click does not work you may alternatively open the file by dragging it into the MATLAB command window.

- After the installation is done the Risk-neutral Density Fitting Tool icon will be listed among your MATLAB Apps.

- If the installation does not work switch to the next method.

Installing rdnfittool through zip archive

- Download the zip archive containing all the necessary resources.

- Extract the archive contents into a local folder.

- Set the folder containing the extracted file as MATLAB current folder or, alternatively, add it to the MATLAB path list.

- Type

rndfittoolto run the tool.

Quick usage

- Load input data. Native formats from OptionMetrics and CBOE are supported (see next section).

- Infer risk-neutral mean and variance through

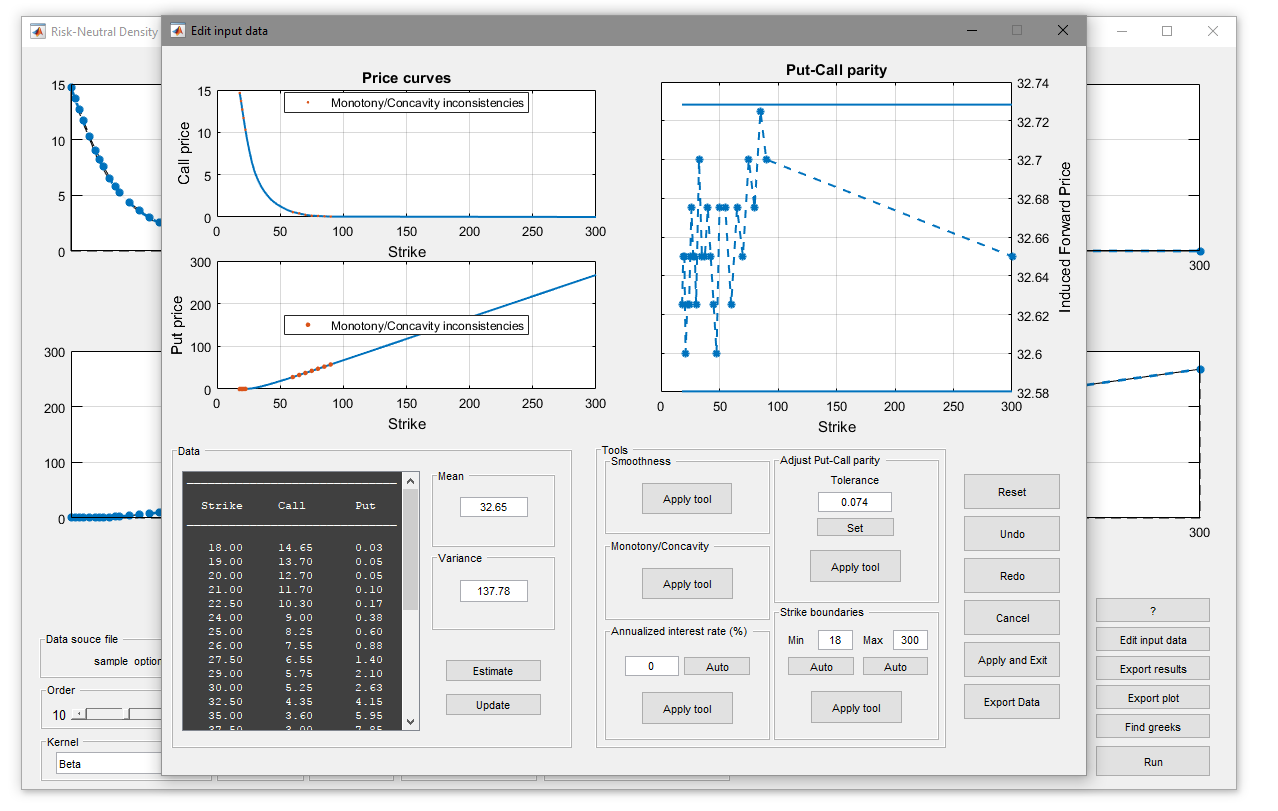

Edit input data. PressEdit input datato validate your changes. Change strike boundaries (you may need to repeat this step in case the fitting is not satisfactory). PressApply toolandApply and Exitto save all changes and return to the main window.

- Choose order (e.g. 11), kernel (e.g. Gen. Weibull) and method (e.g. PCA, 99%, constrained).

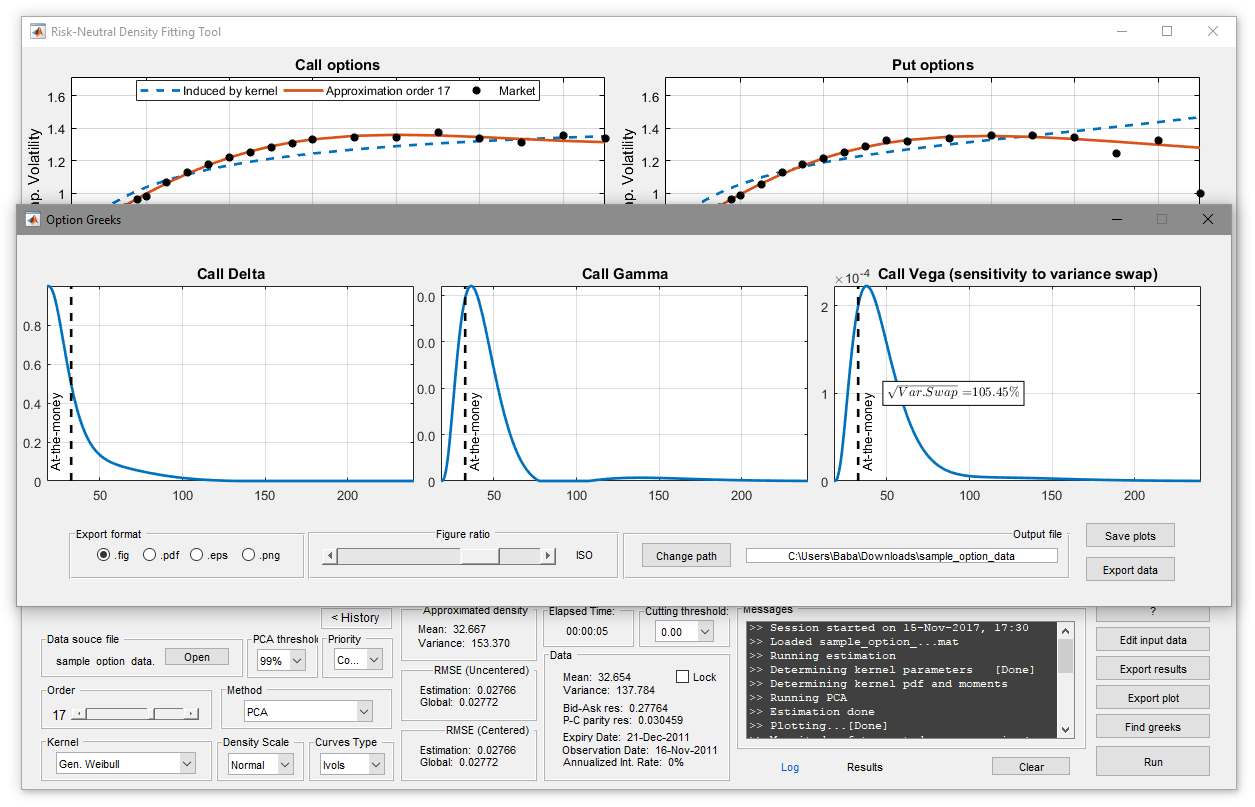

- Press

Find greeksto compute the Greeks (still model-free).

- All plots and results can be exported through

Export plotsandExport results.

Supported data sources

The standard format for input data is a MAT-file (see this sample) with the following structure

Variable name: [Size Type]

K: [Mx1 double] %%%%%%

call: [Mx1 double] % Mandatory

put: [Mx1 double] %

m: [2x1 double] %%%%%%

obsDate: [1x6 int] %%%%%%

expDate: [1x6 int] %

call_a: [Mx1 double] % Optional

call_b: [Mx1 double] %

put_a: [Mx1 double] %

put_b: [Mx1 double] %%%%%%

Required variables:

Kvector of strike valuescallvector of observed call pricesputvector of observed put pricesmvector containing guessed mean and variance (can be set to [])

Optional variables:

obsDateobservation date in numeric format ‘yyyy mm dd’expDateexpiry date in numeric format ‘yyyy mm dd’call_avector of call ask pricescall_bvector of call bid pricesput_avector of put ask pricesput_bvector of put bid prices

External sources

Input data can also be loaded from external sources and optionally converted into compatible MAT-file forma through Edit input data. However, loading MAT-formatted data is normally faster.

OptionMetrics

The data must have .xls, .xlsx or .csv extension and be formatted with all options (e.g. date format) set to the default values provided in the OptionMetrics download page. The dataset must contain all the information related to the mandatory variables. Possibly unrequired fields can be safely appended at any position of the spreadsheet, if needed. Options with several maturities and/or observation dates can be collected into the same file. If this is the case, the user will be asked to choose a maturity when loading data.

CBOE

The data may be saved either into default .dat format available at CBOE website or be pre-converted into .xls/.xlsx format. The dataset must contain all the information related to the mandatory variables. Possibly unrequired fields can be safely appended at any position of the spreadsheet, if needed. If this is the case the user will be asked to choose a maturity when loading data.

Note: The CBOE format changed on 26/11/2018. The new format is supported only in the latest version of rndfittool.